HRAs and Medicare Reimbursement

October 22, 2020 | HRA OCA News Quick Alerts

Understanding when Medicare reimbursements are permissible

Employers often ask questions regarding employer paid reimbursement of Medicare premiums and/or payment/reimbursement of unreimbursed medical expenses of Medicare beneficiaries.

This blog will help identify the circumstances under which a Medicare reimbursement is permissible under both Medicare’s secondary payor rules (“MSP Rules”) and the ACA’s Health Insurance Reforms.

Employers paying or reimbursing an active employee’s Medicare premiums has always raised issues under Medicare’s secondary payor rules (“MSP Rules”). Beginning in 2013, more specifically with the issuance of Notice 2013-54, such payments/reimbursements for active employees also raised issues under the ACA’s health insurance reforms. In fact, the ACA’s health insurance reforms, as interpreted by the agencies in Notice 2013-54, prohibited payment/reimbursement by the employer of an active employee’s Medicare premiums in virtually all circumstances (even when MSP Rules did not apply). The good news is that the DOL’s and the IRS’ interpretation of the ACA’s health insurance reforms has, to some extent, evolved since 2013–in large part due to pressure from the Trump administration and legislation by Congress.

Now, there are several situations in which an employer can pay or reimburse an active employee’s Medicare premiums. For example, Congress created Qualified Small Employer Health Reimbursement Arrangements (QSHERAs) in 2016 that are available to small employers (those less than 50 full-time equivalents in the prior calendar year). We now also have Individual Coverage Health Reimbursement Arrangements (ICHRAs) that are available to employers of any size—and other opportunities. But even though opportunities exist, those opportunities are still limited. More importantly, the landscape now is extremely complex, due in large part to the employer size requirements under the MSP Rules, but also on account of the fact that such arrangements must satisfy BOTH the MSP Rules and the ACA’s health insurance reforms. To help ease the analysis, we have identified in the below chart the various types of reimbursement arrangements (which we refer to as “HRAs”) sponsored employers of various sizes that will satisfy both the MSP Rules and the ACA.

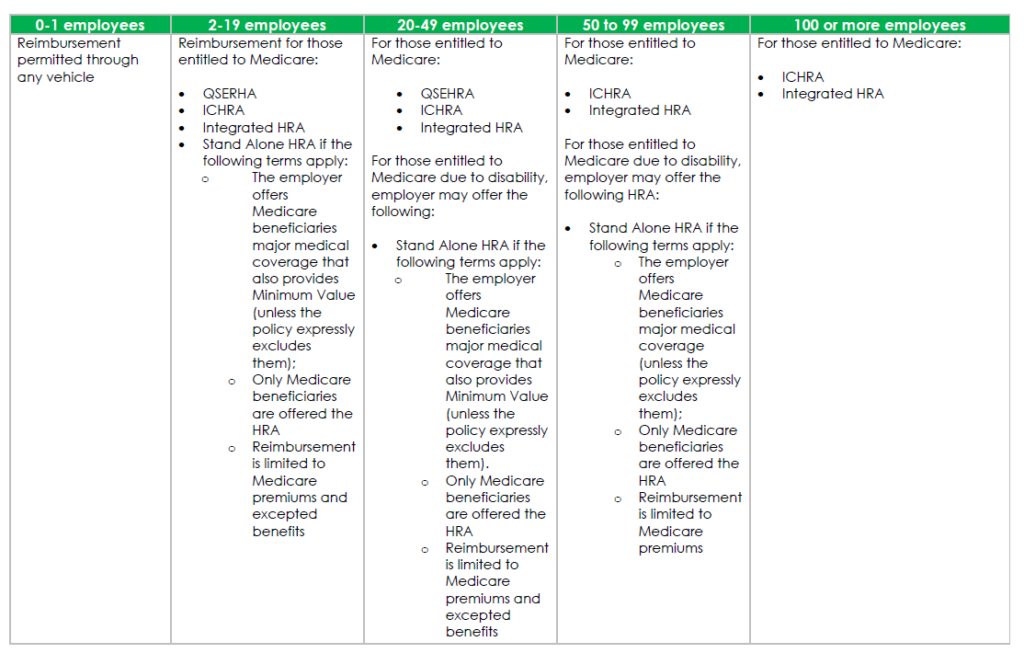

Medicare Reimbursement Chart

The chart below identifies the circumstances under which a Medicare reimbursement is permissible under both Medicare’s secondary payor rules (“MSP Rules”) and the ACA’s Health Insurance Reforms.

The chart is also based on the following terms and assumptions.

- All HRAs are subject to additional rules and regulations applicable to that particular type of HRA. For example, ICHRAs offered to one ore more employees in a specified class (e.g. full-time) must be offered to all employees in that class, including but not limited to those entitled to Medicare and without regard to the reason for such Medicare entitlement.

- Employees eligible for Medicare due to ESRD may not participate in a stand alone HRA (as defined below) until after the 30-month coordination period prescribed by CMS ends.

- This chart does not apply to retirees/former employees. Except for MSP rules for former employees eligible for Medicare due to ESRD who are in the 30-month coordination period prescribed by CMS, neither the MSP Rules nor the ACA’s health insurance reforms apply to the retiree only plans.

- An integrated HRA is an HRA that is only available to those also enrolled in the employer’s major medical plan.

- A “stand alone” HRA is an HRA that does not limit participation to those enrolled in the employer’s major medical plan.

- The stand alone HRA must comply with the applicable opt-out and waiver provisions otherwise required to satisfy the ACA’s integration rules.

- The employer size calculation is subject to the rules and requirements set forth in Medicare.